Have you ever stood in an aisle at the pharmacy or grocery store, staring at an empty shelf where a critical medication or staple item used to be? You aren't alone. In recent years, this frustration has become a global norm. But behind those empty shelves lies a complex web of economic forces known as pricing pressure and supply shortages. These aren't just temporary inconveniences; they are structural shifts that reshape how businesses operate, how governments regulate markets, and ultimately, how much we pay for the essentials of life.

When supply chains break-whether due to geopolitical conflicts, labor strikes, or sudden demand spikes-the result is rarely just higher prices. It creates a ripple effect that touches employment, industrial production, and consumer trust. Understanding these dynamics is no longer optional for economists or business leaders; it is essential for navigating the modern economy.

The Anatomy of a Bottleneck

To understand why prices spike and goods disappear, we need to look at the mechanics of a bottleneck. A bottleneck occurs when one part of the production process cannot keep up with the rest. Imagine a highway where three lanes merge into one. No matter how fast cars travel on the wide road, the single lane limits the total flow. In economics, this happens when production capacity, transportation networks, or labor availability hit a wall.

The Office for Budget Responsibility (OBR) identified these 'demand-driven bottlenecks' as critical factors influencing inflation. This isn't theoretical. During the post-pandemic recovery, specific sectors faced inelastic supply constraints. For example, the energy market saw depleted European gas reserves following a cold winter, combined with surging Chinese demand and unresponsive Russian supply. The result? UK wholesale gas prices skyrocketed to £200 per therm in August 2021, compared to a five-year average of just £35-45. When the input cost for heating and manufacturing jumps fourfold overnight, every downstream product-from plastic packaging to pharmaceuticals-faces immediate pricing pressure.

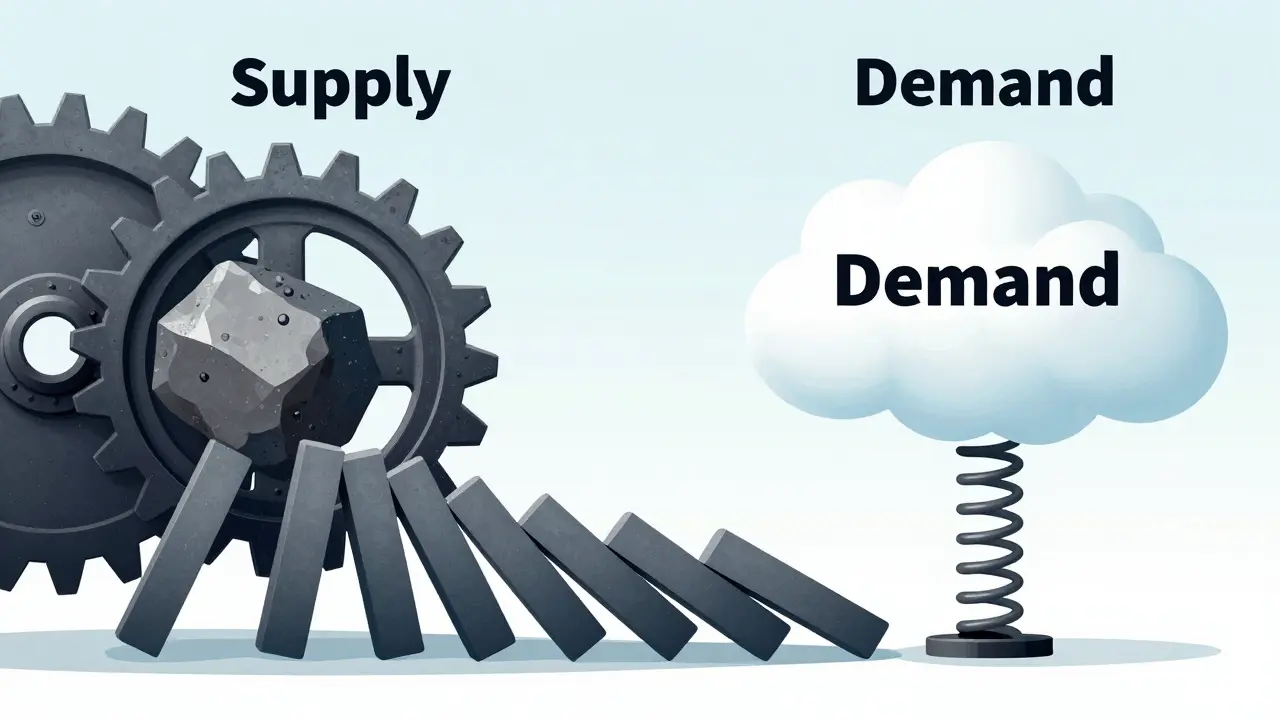

Supply Shocks vs. Demand Shocks: Which Hurts More?

Not all economic disruptions are created equal. Economists distinguish between supply shocks (a reduction in available goods) and demand shocks (a sudden increase in desire for goods). While both drive inflation, their impacts differ significantly.

Research from the Cleveland Federal Reserve offers a stark comparison using structural vector autoregression models. They found that supply shocks have approximately five times greater impact on price levels than demand shocks. Specifically, a supply shock raises the core Personal Consumption Expenditures (PCE) price level by about 0.25%, whereas a demand shock raises it by only 0.05% after three years. Furthermore, supply shocks depress employment more severely (-0.15% vs -0.05%).

| Metric | Supply Shock Impact | Demand Shock Impact |

|---|---|---|

| Price Level Increase (Core PCE) | +0.25% | +0.05% |

| Employment Depression | -0.15% | -0.05% |

| Supplier Delivery Times | Significant Increase | Moderate Increase |

| Primary Driver | Production/Labor Constraints | Consumer Spending Surge |

This data explains why central banks struggle during periods of high supply disruption. Traditional tools like raising interest rates work well to cool down excessive demand, but they do little to fix a broken supply chain. In fact, tightening monetary policy during a supply shock can worsen unemployment without effectively lowering prices, creating a 'stagflation' risk.

The Human Cost: Labor Market Rigidity

Behind every statistic is a human element, particularly in the labor market. Shortages often stem from a mismatch between available workers and needed skills, exacerbated by rigid regulations. The U.S. labor force participation rate remained 1.5 percentage points below pre-pandemic levels through Q2 2022. Why? Because people didn't just want jobs; they wanted different kinds of jobs, and systems were slow to adapt.

The hospitality sector provides a clear example. Labor shortages persisted for over 18 months not because there were no workers, but because of occupational licensing requirements and skill mismatches. Workers who left service roles during lockdowns couldn't easily return due to changed career paths or regulatory hurdles. The OBR noted that government wage support schemes, while well-intentioned, inadvertently reduced labor market flexibility by 12-15% in affected sectors. When workers stay in roles they no longer fit into, productivity drops, and businesses face higher costs per unit of output, driving up prices for consumers.

When Price Controls Backfire

Faced with soaring costs, politicians often turn to price controls, believing they can protect consumers by capping prices. However, economic history shows this usually exacerbates shortages. The Foundation for Economic Education documents that government-imposed price ceilings prevent the natural balancing mechanism of markets. If you cap the price of bread below its production cost, bakers stop baking. Instead of cheaper bread, you get no bread.

A vivid case study occurred in the UK energy market. The government's energy price cap prevented providers from passing rising wholesale costs to consumers. While this shielded households temporarily, it destroyed the viability of smaller competitors. Between August and December 2021, 27 smaller energy providers failed. The burden shifted to larger incumbents and taxpayers, creating long-term instability. Harvard economist Martin Weitzman’s research on 'shortage deformation' predicts exactly this outcome: when prices are held artificially low, consumers engage in speculative hoarding once scarcity becomes apparent, further draining supplies.

Sector-Specific Impacts: From Cars to Chemicals

Pricing pressure does not affect all industries equally. Energy-intensive sectors bear the brunt of raw material shortages. The OBR reported that UK steel, glass, and chemical producers faced input cost increases of 25-40% in Q3 2021. These companies had two choices: absorb the costs and shrink margins, or pass them on to customers and risk losing volume. Most chose the latter, contributing to broader inflation.

The automotive sector offers another lesson. Semiconductor shortages led to a 7.2% decline in U.S. auto production in 2021. Unlike food, cars are durable goods. Consumers delayed purchases, waiting for prices to drop or inventory to return. This behavior created a secondary effect: reduced spending in other areas, such as home improvements or entertainment, slowing overall economic growth. The Institute for Supply Management found that 76% of manufacturing executives reported supply chain disruptions in Q4 2021, with average supplier delivery times jumping from 45 days to 78 days.

Strategic Responses: Resilience Over Efficiency

For decades, businesses prioritized 'just-in-time' efficiency, minimizing inventory to cut costs. Pricing pressures have forced a shift toward 'just-in-case' resilience. Companies are now willing to pay a premium for security.

- Dual-Sourcing: Relying on multiple suppliers for critical components. A McKinsey survey of 500 global companies found that firms with dual-sourcing strategies recovered 35% faster from disruptions.

- Digital Visibility: Investing in real-time supply chain tracking tools reduced inventory stockouts by 28% on average. Knowing where your materials are allows for proactive rerouting rather than reactive panic.

- Nearshoring: Moving production closer to home. Goldman Sachs predicted that nearshoring would reduce supply chain vulnerability by 25% in North America, though it would increase production costs by 8-12% long-term. This trade-off-higher base costs for lower risk-is becoming the new standard.

Gartner projects that 60% of Global 2000 companies will implement 'digital twin' supply chain simulations by 2025. These virtual models allow businesses to test scenarios, such as a port strike or a tariff hike, before they happen, reducing response times by 45%. This technological leap is not just about IT; it is a fundamental change in how economic risk is managed.

Global Inequality in Disruption

The impact of pricing pressure is not distributed evenly across the globe. Emerging markets suffer disproportionately. The International Monetary Fund (IMF) noted that emerging economies experienced 25-30% larger inflationary impacts from supply chain disruptions than advanced economies. Why? Because their supply networks are less diversified and they rely more heavily on imported inputs. When global shipping costs double, a country importing 80% of its energy faces a crisis, while a self-sufficient nation faces a manageable bump.

This disparity fuels geopolitical tension. As nations compete for scarce resources like semiconductors or lithium, cooperation breaks down. The IMF warns that geopolitical fragmentation could keep supply chain pressures 15-20% above pre-pandemic norms through 2025. We are moving from a globalized era of cheap goods to a fragmented era of secure, but expensive, goods.

Looking Ahead: The New Normal

By mid-2023, the San Francisco Federal Reserve reported that supply chain pressure indices had returned to pre-pandemic levels. Does this mean the problem is solved? Not entirely. The acute phase of congestion has passed, but the structural changes remain. Businesses have learned that efficiency without resilience is fragile.

We are entering an era where higher baseline prices may persist due to these strategic shifts. Nearshoring adds cost. Dual-sourcing adds administrative overhead. Digital twins require investment. These are necessary expenses to avoid the chaos of empty shelves, but they contribute to a higher floor for inflation. Policymakers and consumers must adjust expectations accordingly. The goal is no longer rock-bottom prices, but reliable access. Understanding this shift is key to making informed decisions, whether you are investing in stocks, managing a household budget, or shaping public policy.

What is the difference between pricing pressure and inflation?

Inflation is the general increase in prices across an economy over time. Pricing pressure is the specific force driving those increases, often caused by supply shortages, rising input costs, or constrained labor markets. Think of pricing pressure as the engine and inflation as the speedometer reading.

Why do supply shocks hurt employment more than demand shocks?

Supply shocks, such as a lack of raw materials or workers, directly prevent production. If you can't make the product, you don't need the workers to make it, leading to layoffs. Demand shocks simply mean fewer sales, which might lead to reduced hours but not necessarily immediate job losses if the workforce remains employable.

How do price controls affect shortages?

Price caps often worsen shortages by preventing prices from signaling scarcity. When prices are artificially low, demand outstrips supply, leading to panic buying and hoarding. Suppliers may also exit the market if they cannot cover costs, reducing availability further.

What is 'nearshoring' and why is it increasing costs?

Nearshoring involves moving manufacturing closer to the consumer market, often from Asia to neighboring countries. While it reduces supply chain risks and delays, labor and operational costs are typically higher in nearby developed nations, leading to an estimated 8-12% long-term increase in production costs.

Will supply chain pressures return to pre-pandemic levels permanently?

While acute congestion has eased, structural pressures remain. Geopolitical fragmentation, climate-related disruptions, and a strategic shift toward resilience over pure efficiency suggest that supply chain costs will remain 15-20% above pre-pandemic norms through 2025, according to IMF projections.